Goal: Learn how to audit your portfolio, identify imbalances, and rebalance strategically to stay aligned with your financial objectives.

Why Review & Rebalance?

– Market Movements: Stocks, bonds, and gold perform differently over time, skewing your original allocation.

– Example: If equity grows from 60% to 75% of your portfolio, your risk exposure increases.

– Life Changes: New goals (marriage, child’s education), income shifts, or risk tolerance changes.

– Tax Optimization: Harvest tax losses or minimize capital gains.

Step 1: Review Your Portfolio

1. Check Performance vs. Goals

– Compare Returns: Use tools like Kuvera or ET Money to track:

– Absolute returns (e.g., ₹10L → ₹12L in 1 year).

– Relative returns (vs. benchmarks like Nifty 50).

– Example: If your portfolio grew 8% but Nifty 50 grew 12%, you may need to adjust holdings.

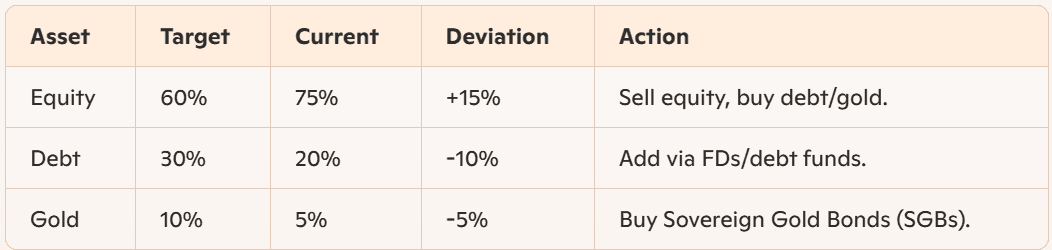

2. Analyze Asset Allocation

Current vs. Target Allocation:

3. Evaluate Individual Holdings

– Underperformers: Sell stocks/funds lagging peers (e.g., HDFC Bank vs. ICICI Bank).

– Overconcentration: Avoid >10% in a single stock (e.g., Reliance Industries dominating your portfolio).

4. Tax Implications

– Capital Gains: Selling equity <1 year → 15% tax; >1 year → 10% tax on gains >₹1L.

– Tax-Loss Harvesting: Offset gains by selling loss-making investments (e.g., sell Zomato at a loss to reduce taxes on Infosys gains).

Step 2: Rebalance Your Portfolio

1. Decide Frequency

– Time-Based: Quarterly, biannually, or annually.

– Threshold-Based: Rebalance when an asset deviates >5% from target (e.g., equity crosses 65% in a 60% target).

2. Rebalancing Strategies

– Sell High, Buy Low: Trim overperforming assets (equity) to fund underperformers (debt/gold).

– Redirect New Investments: Allocate fresh SIPs to underweight assets (e.g., add more debt funds).

– Use Dividends: Reinvest dividends from equity into debt/gold.

3. Tools for Rebalancing

– Automated Platforms: Use robo-advisors (e.g., Scripbox, ET Money) for auto-rebalancing.

– Manual Adjustments: Platforms like Zerodha or Groww let you rebalance with a few clicks.

Case Study: Rebalancing an Indian Portfolio

Original Allocation (2022):

– Equity: 60% (Nifty 50 Index Fund)

– Debt: 30% (PPF + Corporate Bond Fund)

– Gold: 10% (SBI Gold ETF)

2023 Performance:

– Equity surged 25% → now 70% of portfolio.

– Debt grew 7% → now 25%.

– Gold dropped 3% → now 5%.

Rebalancing Actions:

1. Sell ₹1.5L equity to book profits.

2. Invest ₹1L in debt (e.g., HDFC Corporate Bond Fund).

3. Buy ₹50k in Sovereign Gold Bonds (SGBs).

Result: Back to 60% equity, 30% debt, 10% gold.

Common Mistakes to Avoid

– Over-Rebalancing: Frequent tweaks increase costs and taxes.

– Ignoring Taxes: Selling equity within a year triggers short-term capital gains.

– Emotional Decisions: Holding overperforming stocks due to greed (e.g., Adani stocks in 2022).

FAQs for Indian Investors

– “How often should I rebalance?”

Once a year or when allocation deviates >5% (e.g., equity crosses 65% in a 60% target).

– “What if I don’t want to sell investments?”

Redirect new SIPs to underweight assets (e.g., pause equity SIPs, start debt SIPs).

– “Best debt options for rebalancing?”

PPF (tax-free), corporate bond funds, or FDs (for short-term needs).

Tasks for You.

1. Audit Your Portfolio:

– Use Coin by Zerodha to check current allocation vs. target.

– Example: If equity is 75% vs. 60% target, calculate how much to sell.

2. Rebalance Strategically:

– Sell ₹10k of equity and buy debt/gold (start small if hesitant).

– Update SIPs: Shift ₹5k/month from equity to debt funds.

3. Set Reminders:

– Mark your calendar for quarterly/ annual reviews.

Key Takeaways

1. Discipline > Timing: Regular rebalancing beats chasing market highs/lows.

2. Tax Efficiency: Use tax-loss harvesting and long-term holding periods.

3. Stay Flexible: Adjust targets for life changes (e.g., reduce equity as you near retirement).

Your article helped me a lot, is there any more related content? Thanks!

Thanks for sharing. I read many of your blog posts, cool, your blog is very good.