Goal: Learn to invest in gold strategically using tax-efficient, low-cost instruments instead of physical gold.

Why Invest in Gold?

– Inflation Hedge: Gold retains value when currencies weaken (e.g., ₹1L in gold in 2010 = ₹4.3L today).

– Portfolio Diversification: Uncorrelated with stocks (safe haven during crashes).

– Liquidity: Easier to sell than real estate.

Indian Context:

– Gold is culturally significant but physical gold (jewelry, coins) has high making charges (6–14%) and storage risks.

– Modern options like SGBs and Gold ETFs solve these issues.

Key Gold Investment Options in India

1. Sovereign Gold Bonds (SGBs)

– What? Government-backed bonds where you own “paper gold.”

– Features:

– Interest: 2.5% p.a. on initial investment (paid semi-annually).

– Capital Appreciation: Linked to gold price.

– Tax Benefits: No capital gains tax if held until maturity (8 years).

– Example: Invest ₹1L in SGBs → Earn ₹2.5k/year interest + gold price gains (tax-free at maturity).

How to Buy:

– RBI issues tranches (check RBI website).

– Buy via banks, brokers (Zerodha), or stock exchanges (secondary market).

2. Gold ETFs

– What? Exchange-traded funds tracking gold prices.

– Features:

– Low Cost: Expense ratio ~0.1–0.5% (vs. 6% jewelry making charges).

– Liquidity: Trade like stocks (NSE/BSE).

– Examples:

– SBI Gold ETF (0.5% fee).

– Nippon India Gold ETF (0.1% fee).

How to Buy:

– Open a Demat account (Zerodha, Groww) → Search “GOLDBEES” (Nippon ETF ticker).

3. Digital Gold

– What? Buy/sell fractional gold online via apps.

– Features:

– Low Minimum: Start with ₹1.

– Storage: Vaulted by MMTC-PAMP or SafeGold.

Platforms:

– Paytm Gold (₹1 minimum).

– SafeGold (backed by Reliance).

Caveat: Not as tax-efficient as SGBs; capital gains taxed like physical gold.

4. Gold Mutual Funds

– What? Invest in Gold ETFs via SIPs (no Demat needed).

– Examples:

– Axis Gold Fund (0.3% fee).

– HDFC Gold Fund (0.5% fee).

How to Buy: Via mutual fund platforms (ET Money, Coin by Zerodha).

5. Physical Gold (Jewelry/Coins)

– Pros: Cultural utility (weddings, gifts).

– Cons:

– High making charges (6–14% loss upfront).

– Risk of theft, no passive income.

– Taxation: Short-term gains (<3 years) taxed at slab rate; LTCG taxed at 20% with indexation.

Comparison of Gold Instruments

How to Invest in Gold (Step-by-Step)

1. Choose Your Instrument:

– Long-Term/Safety: SGBs (tax-free, interest income).

– Short-Term/Liquidity: Gold ETFs.

– Convenience: Digital gold (fractional ownership).

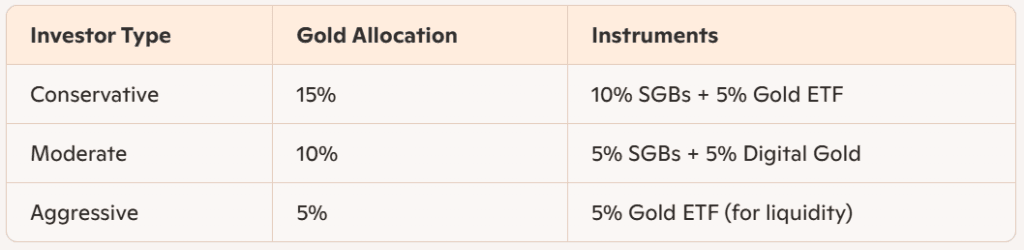

2. Allocate Smartly:

– Conservative Portfolio: 10–15% in gold.

– Aggressive Portfolio: 5–8% in gold.

3. Buy:

– SGBs: Apply during RBI tranches via Zerodha/ICICI Bank.

– ETFs: Buy “GOLDBEES” via Zerodha/Groww.

– Digital Gold: Use Paytm/PhonePe apps.

Taxation of Gold in India

Physical/Digital Gold/ETFs:

– Short-Term (<3 years): Taxed at income slab rate.

– Long-Term (≥3 years): 20% tax with indexation.

SGBs:

– Interest: Taxed at slab rate.

– Capital Gains: Tax-free if held until maturity (8 years).

Example:

– Buy ₹1L SGBs → Sell after 8 years at ₹2L → Tax-free profit of ₹1L.

Tasks for Day 22

1. Buy SGBs/ETFs:

– Invest ₹1,000 in SGBs via Zerodha (secondary market) or ₹500 in Gold ETFs (GOLDBEES).

2. Compare Returns:

– Use Value Research to check 5-year returns of SBI Gold ETF vs. physical gold.

3. Audit Physical Gold:

– Calculate making charges on jewelry (e.g., 10% loss on ₹50k necklace = ₹5k gone).

Key Takeaways

1. Avoid Physical Gold: High hidden costs (making charges, storage).

2. SGBs > ETFs for Long-Term: Tax-free maturity + interest income.

3. Rebalance Annually: Maintain 5–15% gold allocation.

FAQs for Indian Investors

– “Are SGBs safe?”

Yes! RBI-backed, sovereign guarantee.

– “Can I exit SGBs early?”

Yes, after 5 years on exchanges, but taxed as LTCG.

– “Best time to buy gold?”

Dip during festivals (e.g., Dhanteras) or global uncertainty (geopolitical tensions).

Sample Gold Allocation