Your goal involves determining how to properly analyze GDP alongside inflation rates and interest rates to enhance your investment plans.

Why Macro Matters?

Nationally relevant trends influence both business sector financial results and driving market attitudes.

For example:

High inflation → RBI raises interest rates → Bank stocks rally, but real estate suffers.

GDP growth slowdown → Cyclical sectors (auto, cement) underperform, while defensives (FMCG, pharma) thrive.

Several important macroeconomic indicators guide Indian investors in their investment choices

1. GDP Growth Rate

Economic output consisting of goods and services constitutes the metric which this indicator evaluates.

Impact on markets:

– High GDP growth (e.g., 7%+): Boosts cyclical stocks (infrastructure, banks).

A GDP growth rate of 4% attracts investors to buy sections of the market with defensive characteristics (IT and FMCG).

The Indian economy achieved a GDP growth rate of 6.1% during the first quarter of 2023 which led to increased buying of auto and capital goods stocks.

2. Inflation (CPI & WPI)

The Consumer Price Index (CPI) measures how retail prices change affecting food costs fuel expenses alongside housing expense rates.

Higher consumer price index numbers of more than six percent prompts RBI to elevate repo rates which subsequently raises bond yields and damages debt fund returns.

CPI reached 7.8% during 2022 and the Reserve Bank of India raised repo rate to 6.5% which resulted in Bank Nifty reaching a 15% increase.

– Wholesale Price Index (WPI): Measures wholesale inflation (raw materials).

During 2023 Asian Paints faced declining profit margins because the increasing Wholesale Price Index intensified their production costs.

3. RBI Monetary Policy (Repo Rate)

The Repurchase (Repo Rate describes the rate RBI applies to grants loans to financial institutions.

The Reserve Bank of India increasing its repo rate generates advantages for banks through better lending margins while it leads to financial burdens for real estate sectors along with NBFCs.

When the repo rate declines the market experiences increased borrowing along with growth stock stimulation.

The realty sector stocks DLF and Godrej Properties experienced increased performance after the Reserve Bank of India maintained the.repo rate at 6.5% (2023).

4. Fiscal Deficit

The indicator measures the relationship between government expenses and financial income.

High deficit (>6% of GDP): Raises borrowing costs, pressures infrastructure stocks.

Example (2021): Fiscal deficit at 9.5% → Bond yields spiked, PSU banks underperformed.

5. Current Account Deficit (CAD)

The measurement of India’s trade gap between imports and exports .

what this indicator reveals.

High CAD: Weakens rupee → IT/exporters (Tata Motors, Infosys) benefit.

Trade Deficit: A widening CAD often indicates a larger trade deficit, which can lead to currency depreciation and inflationary pressures.

Economic Growth: A high CAD can limit economic growth by diverting domestic savings towards financing imports rather than investments.

Foreign Exchange Reserves: A persistent CAD can reduce foreign exchange reserves, making it harder for the country to meet its external obligations.

6. Unemployment Rate

– High unemployment: Reduces consumer spending → Impacts retail, auto sectors.

The rise of unemployment to 23% during lockdowns led to Maruti Suzuki sales experiencing a 47% decrease.

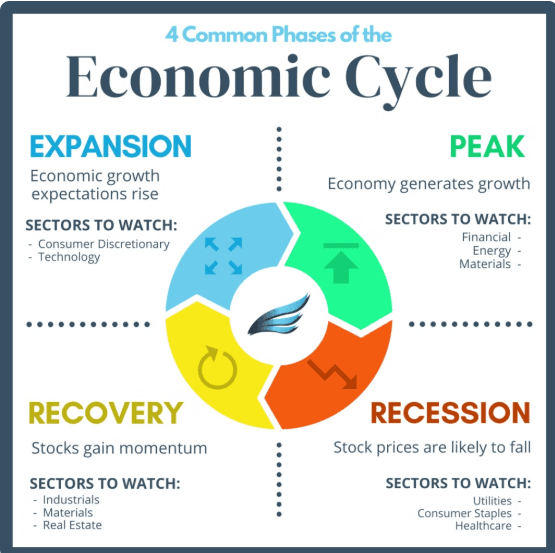

How to Use Macro Data in Your Strategy

1. Sector Allocation

– Expansionary Economy (High GDP): Overweight cyclicals (banks, infrastructure).

Recessionary signs lead investors to switch into defense stocks such as pharmaceuticals and utilities.

2. Debt vs. Equity Balance

High inflation and rising interest rates signal market conditions which warrant debt fund reduction because bond prices decline.

– Low Rates/Stable Inflation: Increase equity allocation.

3. Currency Hedging

– Weak Rupee: Invest in export-heavy sectors (IT, pharma).

The strong value of the Indian rupee enables oil marketing companies and other import-oriented businesses to do better (such as IOCL and others).

Tasks for You.

1. Track Macro Data:

– Bookmark RBI Monetary Policy Dashboard and Ministry of Statistics.

Plan to record both the future RBI policy announcement date along with the GDP publication date.

2. Analyze Past Trends:

Evaluate the behaviour of Nifty 50 throughout the period of high inflation in 2022 against the regime of low inflation that occurred in 2020.

Investors should compare Information Technology sector returns during the time when the currency depreciated from ₹75/$ to ₹83/$ against periods of appreciation.

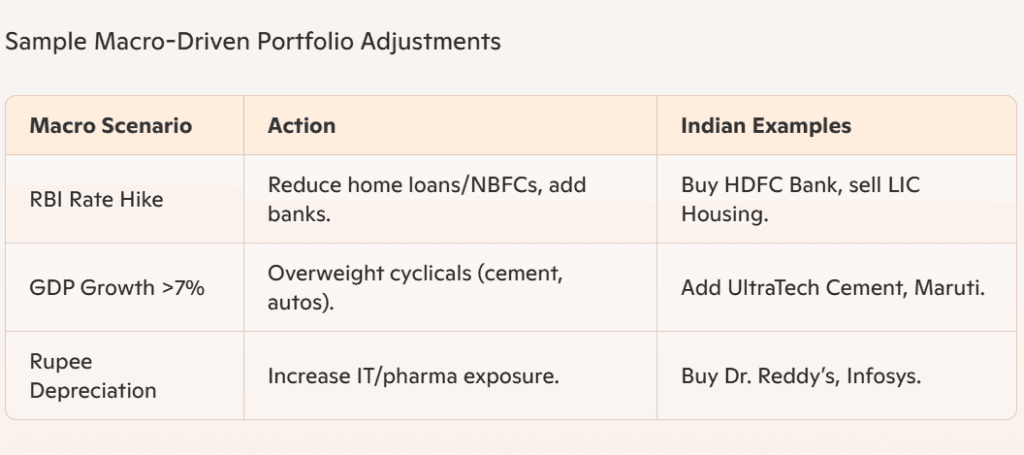

3. Adjust Your Portfolio:

The signal of upcoming rate cuts from RBI should trigger acquisitions of sensitive rate stocks such as HDFC Bank and L&T.

The Boyd analyst would implement a trading adjustment by allocating more funds toward Information Technology stocks especially TCS and Infosys.

Key Takeaways

1. The market-relevant decisions on repo rates from RBI along with fiscal policy actions guide the financial landscape.

2. When economic cycles change invest across different sectors where the economy is in its growth phase (for example infrastructure).

3. U.S. Federal Reserve policy changes together with oil price movements influence Indian macro conditions through indirect means.

Common Mistakes to Avoid

The CPI data from one month does not establish patterns beyond the current moment.

The U.S. recession predictions for 2023 brought damage to Indian Information Technology stock market performance.

The rising rates create negative effects on real estate properties but simultaneously generate benefits for banking institutions.

FAQs for Indian Investors

– “Where to find macro data?”

– RBI website, Ministry of Statistics, Trading Economics.

The query about how oil prices impact India appears in this question.

Rising oil costs create a larger CAD deficit which hurts the rupee currency strength and adds pressure to state-owned fuel companies including BPCL along with HPCL.

– “Best sectors during stagflation?”

– Gold (via SGBs), FMCG (Nestlé, HUL), and utilities (NTPC).